4-Point Inspection

A standardized Florida inspection covering the four systems your insurance carrier needs to underwrite an older home: roof, electrical, plumbing, and HVAC. Required by most Florida carriers on homes 25 years or older.

If a Florida carrier is asking for one, you need one.

If you're closing on a Florida home built 25+ years ago, almost every carrier will ask for a 4-Point before binding the policy.

At renewal, your carrier may request an updated 4-Point. A current report keeps your policy in good standing.

Knowing what an underwriter will see (and what you can fix beforehand) avoids surprises during closing.

Four systems. Documented in detail.

Each pillar is photographed, conditions are noted, and the report is delivered in the standard format Florida carriers accept.

Roof

Material, approximate age, slope, visible damage, signs of leaks, flashing condition, and remaining useful life.

- Material and age

- Visible damage and wear

- Flashing and penetrations

- Active or past leak indicators

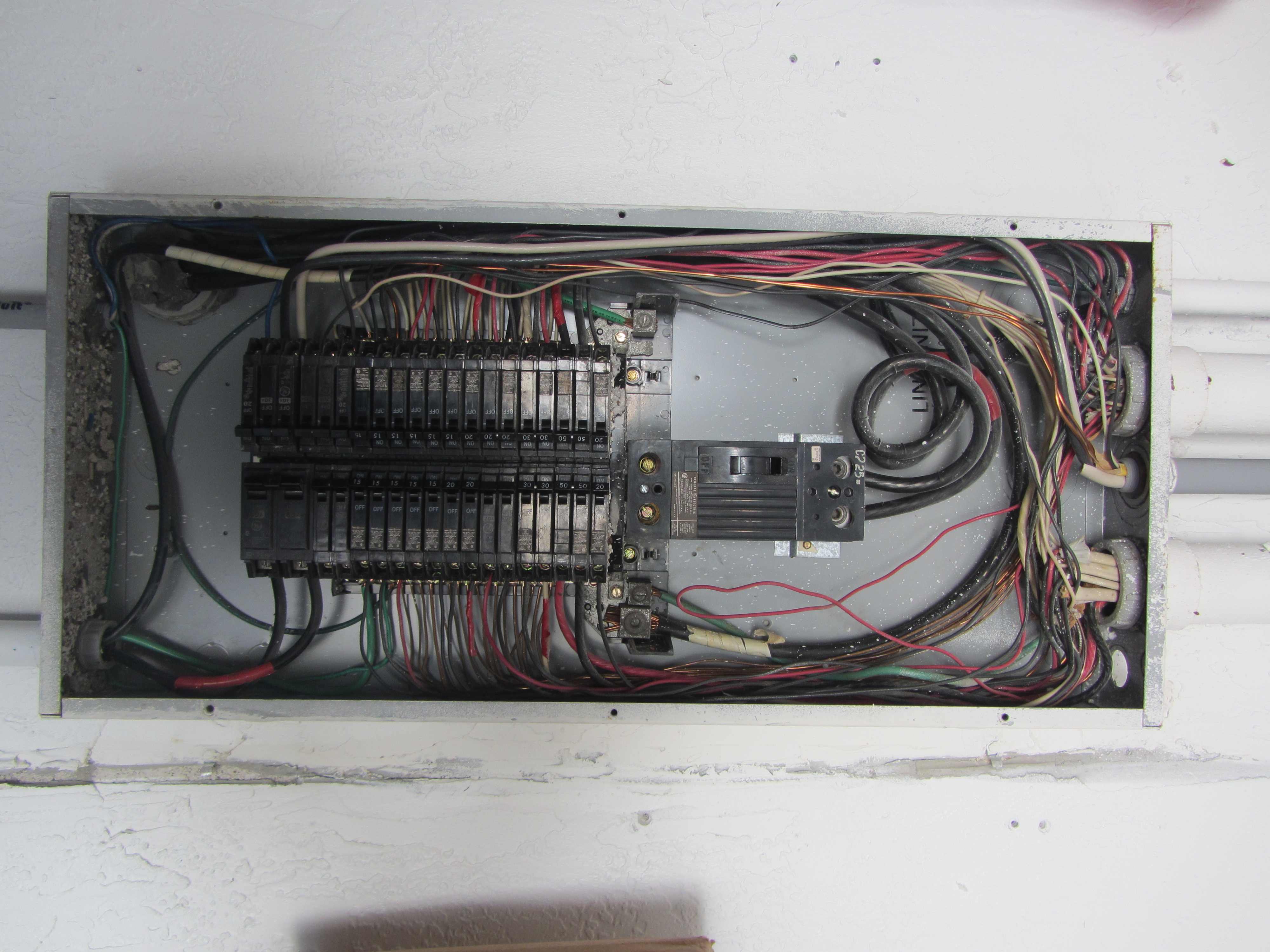

Electrical

Panel manufacturer and age, breaker condition, wiring type (copper vs. aluminum), GFCI/AFCI protection, and any insurer-flagged panels.

- Panel age and manufacturer

- Breakers and bus condition

- Branch wiring type

- Federal Pacific, Zinsco, FPE flags

Plumbing

Pipe material, water heater age and condition, signs of past or active leaks, drainage, and shut-off accessibility.

- Supply and drain materials

- Water heater age

- Active or past leak indicators

- Polybutylene flag (if present)

HVAC

Air handler and condenser age, refrigerant lines, condensate drain, and overall condition. Florida carriers care about end-of-life systems.

- System age and condition

- Refrigerant line wear

- Condensate drainage

- Visible corrosion or rust

More than a hoop to jump through.

A clean 4-Point can be the difference between a written policy and a denied application. A thoughtful one tells you what to address before the underwriter sees it.

When something does come up, we explain it on the call. What it actually means, who can fix it, and roughly what's involved.

A clear 4-Point report makes it easy for an underwriter to bind your policy. An ambiguous or incomplete one stalls things.

Carriers occasionally request a fresh 4-Point at renewal. Having a current report ready avoids non-renewal scrambles.

A pre-listing 4-Point lets sellers fix what would otherwise become a buyer credit. Buyers use it to negotiate or walk if a deal-breaker shows up.

A short list before we arrive.

A few minutes of prep saves us a return trip. We send a checklist after scheduling, but here's the gist.

- Clear access to the electrical panel

- Clear path to the water heater

- Attic hatch unobstructed and openable

- HVAC closet or pad accessible

- Pets secured in a separate room

- System ages handy if you know them

- Tenant notified (if applicable)

- Gate, lockbox, and entry codes shared

A signed report your insurance carrier accepts.

PDF emailed to you, with a copy sent to your agent on request. Photos of every pillar, condition notes, and a summary of anything that's likely to draw underwriter attention.

- Standard Florida 4-Point format

- Photos of roof, panel, plumbing, HVAC

- Condition notes and remaining useful life

- Underwriter-relevant flags called out

- Signed by State Certified inspector

From request to report in a few days.

-

01

Request & confirm

Submit the request form. Luis confirms the appointment by phone or text the same day.

-

02

On-site inspection

45 to 90 minutes covering all four systems. You're welcome to walk along.

-

03

Report delivery

Same-day PDF to you and your agent. Phone walk-through to explain what's in it.

4-Point inspections across the territory.

South and Central Florida, anywhere south of Seminole County. Featured pages for the four counties where we work most.

Why do Florida insurers require a 4-Point Inspection?

Florida carriers use the report to assess underwriting risk on the four systems most likely to cause claims: aging electrical panels, failing plumbing, end-of-life HVAC, and roofs nearing the end of their useful life.

How long does a 4-Point Inspection take?

Typically 45 to 90 minutes on site. The report is delivered the same business day in most cases.

What if my 4-Point report shows issues?

The report doesn't pass or fail. It documents the actual condition. If something is likely to cause underwriting trouble, we explain what your insurer is likely to flag and what fixing it would involve.

Do you send the report directly to my insurance agent?

Yes. Provide your agent's email when you submit the request and we'll send a copy directly. You'll be cc'd.

Get your 4-Point booked.

A few details about your property and your preferred date. Most reports back the same business day.